10 Charts That Challenge the “Housing Crash Is Over” Narrative

When the average Canadian home price fell from roughly $837,000 at its peak to about $690,000, many celebrated.

Headlines declared that the market was correcting.

Buyers were told affordability was slowly being restored.

With eight rate cuts rolled out over the past cycle, optimism began creeping back into the narrative.

But beneath the surface, the math tells a harsher story.

Yes, prices have declined in nominal terms — about $147,000 nationally from peak levels in early 2022.

However, when adjusted for inflation, the drop looks far steeper in certain regions.

Markets like Hamilton and the Greater Toronto Area have seen inflation-adjusted declines approaching 30–40%.

On paper, that sounds dramatic.

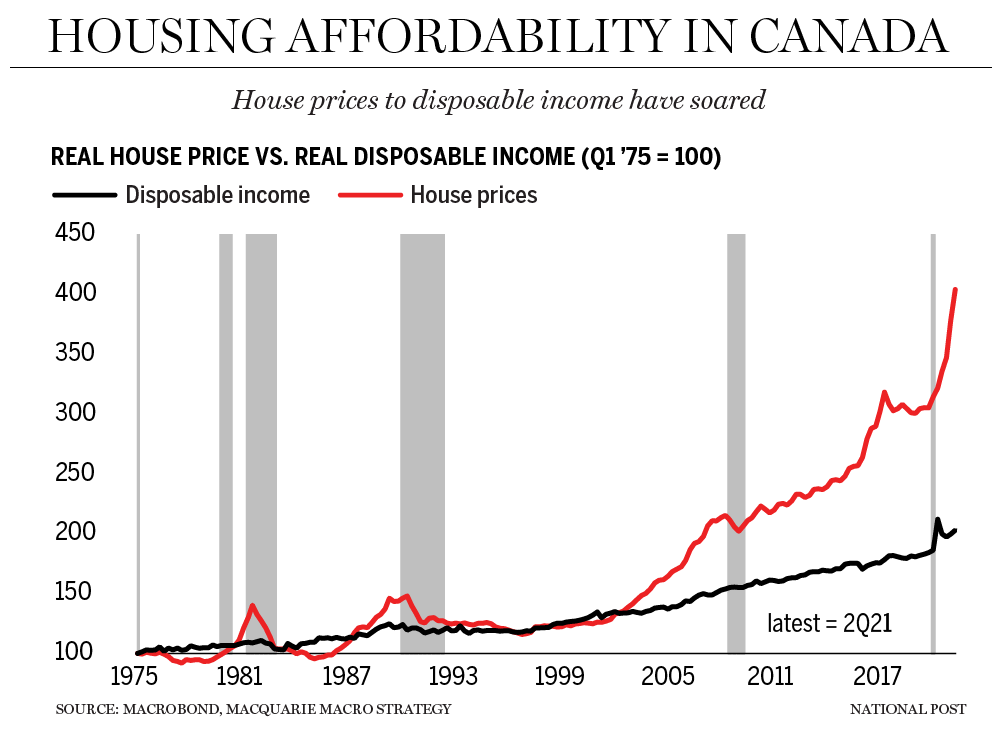

Yet affordability has not meaningfully improved.

The reason lies in how Canadians actually qualify for homes.

Mortgage lenders rely heavily on a metric known as the Gross Debt Service (GDS) ratio.

In simple terms, households generally cannot spend more than about 40% of their gross income on housing costs — including mortgage payments, taxes, and heating.

When you compare median incomes to median home prices using current rates and standard 25-year amortizations, the reality becomes clear.

In cities like Vancouver and Toronto, the cost of servicing a typical home has consumed as much as 85% to 100% of a median household’s income at peak levels.

Even with recent price declines and rate cuts, those markets remain far beyond what average earners can reasonably afford.

This explains why sales activity has stayed weak despite monetary easing.

Since the rate-cut cycle began, many expected buyers to flood back into the market.

Instead, sales volumes have remained historically low.

In fact, current trends suggest transactions in major markets like Toronto could hit levels not seen in three decades.

At the same time, new listings have continued to rise.

That growing gap between listings and sales signals a softer market.

More sellers are entering, but buyers are not absorbing supply at previous rates.

While some hoped lower interest rates would quickly revive activity, affordability constraints and economic uncertainty have muted demand.

And the broader economy adds another layer of complexity.

Canada’s economic structure is unusually tied to real estate.

Residential investment accounts for roughly 8% of Canada’s GDP — double the U.S. share of about 4%.

That means housing plays an outsized role in driving growth.

When the market booms, Canada benefits disproportionately.

But when it slows, the drag is equally amplified.

In practical terms, Canadians devote more of their financial capacity to housing-related debt than their American counterparts.

That leaves less room for spending elsewhere, particularly during periods of rising rates or economic weakness.

Meanwhile, mortgage delinquencies are rising — though not yet at crisis levels.

Current delinquency rates hover around 0.21%, meaning roughly one in every 476 mortgages is 90 days past due.

This is far below the levels seen during the U.S. housing crash of 2008, when delinquencies surged near 10%.

However, stress is appearing at the margins.

The strain is not concentrated among major banks but rather in private lending channels — individual investors and mortgage investment corporations that took on higher-risk borrowers.

When these lenders initiate “power of sale” proceedings, their priority is recovering capital, not maximizing market value.

That can lead to discounted transactions that reset comparable prices lower.

It creates a subtle downward pressure — one transaction at a time.

Prices tend to be “sticky” on the way down because only highly motivated sellers accept steep discounts.

Others simply withdraw listings and wait.

This dynamic slows the correction but does not eliminate it.

Yet perhaps the most significant risk lies not in today’s weakness — but in tomorrow’s supply.

New condominium construction has slowed dramatically, particularly in the Greater Toronto Area and Hamilton.

Pre-construction sales have plunged, in some cases by 80–90%.

Developers are shelving projects amid high costs and uncertain demand.

In five to seven years, this could translate into a sharp supply shortage.

Adding to the pressure are rising development charges.

In Toronto, municipal fees per unit have climbed from roughly $100,000 in 2022 to nearly $140,000 — a 40% increase in just two years.

Those costs ultimately get pᴀssed on to buyers, embedding higher prices into future supply.

At the same time, construction trends are shifting.

Purpose-built rental projects are replacing many condominium developments.

While this may stabilize rental markets over time, it reduces the stock of homes available for individual ownership.

Freehold housing — townhomes, semis, and detached properties — has also stagnated at levels below those seen in the 1990s.

Overlay this with shifting immigration patterns.

Population growth surged during the pandemic recovery, fueling rental demand and price pressures.

If immigration moderates, rental markets could soften — affecting investor demand and broader housing dynamics.

So where does this leave Canada?

The narrative that “the worst is over” may be premature.

Sales remain weak.

Affordability remains strained.

The economy is closely tethered to a cooling housing sector.

Delinquencies are edging up at the fringes.

At the same time, a future supply crunch is quietly forming — one that may reignite upward pressure years from now.

The correction is real.

But the crisis is not simply about falling prices.

It is about structural affordability, economic dependence on housing, shifting supply pipelines, and policy decisions that ripple years into the future.

The biggest misconception may not be that prices fell — but that falling prices alone solve the problem.